Trading Case

XR2

Case Objectives

To understand using options and futures to manage

currency risk; to understand options trading strategies in an environment in

which exchange rate crises exist. Finally,

to gain experience working with a derivative trading support system.

Key Concepts

Currency option and futures pricing; option hedge

parameters; implied volatility shifts.

Case

description

Currency markets can

experience very volatile periods. For

example, in the 1992 European currency crisis the implied volatility for sterling/dollars and dm/dollars jumped from

the 11-12% range in August 1992 to in excess of 20% by October 1992 and then

fell back sharply to above historic levels.

A study by a

In this trading case you

will face the problem of managing exchange rate risk in a currency crisis.

That is, during each trading trial a currency crisis will occur at some

point in time which is marked by a sharp increase in volatility. Although, the timing and the duration of the

crisis is random, prices in the options markets will only provide signals that

volatility is expected to increase near the time of the realized increase.

You will compete against

other traders in the FTS markets by earning grade

cash with respect to a conversion scheme that is designed to both reward

you for seeking out higher returns but penalize you for dropping below an

acceptable floor.

The operational details

of this trading case are the same as for XR1.

The major difference is that a significant shift in volatility will

occur at some time during the trading year (trial).

Trading

Screen

Each trader's screen will

monitor eight markets: the exchange rate, a risk-free bond (strip) with 104

weeks remaining to maturity at the beginning of the period, European call and

put options on the exchange for two different strike prices with a remaining

life of 52 weeks, an exchange rate future contract, and a cash money market.

Definition of A Trading Trial

One trial in this case is

almost 12 months, but time is condensed so that two weeks is equal to “n”

seconds. That is, throughout the trial

trading is continuous but prices will change in discrete time, two week steps

every “n” seconds of FTS time. That is,

in calendar time the markets are open for FTS traders on the first trading day

of every two weeks.

Note: In the

default form of the case “n” seconds equals 20.

The following table

describes price changes in this market:

|

Calendar Time |

Real-time |

|

|

|

|

Day 1, Week 1 |

Time 0-20 seconds |

|

Day 1, Week 3 |

Time 21-40 seconds |

|

Day 1, Week 5 |

Time 41-60 seconds |

|

....................... |

............................... |

New prices are realized

for each trading Day (20 second interval).

Prices reflect the underlying difference in calendar time. That is, the Treasury Strip appreciates

toward its face value over time, and option prices reflect the time left to

maturity etc.

At the end of the year ( = one trading trial), your currency position is

marked-to-market at the prevailing rate.

Market Environment

The first market is the

exchange rate. This is the value of 500 units

of the basket of currencies (bfx) in units of $US. Analyst research has indicated that the

statistical process that approximately describes the behavior of this exchange

rate is a geometric Wiener process with the following properties:

|

Projected |

14%-16% per annum |

|

Spot Index Value (Bid/Ask) |

Near 300 |

|

Projected Drift () |

0.0% per annum |

|

Unit of Time |

2 week (20 seconds) |

|

Eurodollar rate US |

0.03 |

|

Euromark rate |

0.07 |

The projected volatility

is a little above historical averages for volatility but

well below the heights reached in the European currency crisis in 1992.

Securities

And Trading Restrictions

|

Financial Markets |

|

Spot x-rate (500 bfx) in $US (S) |

|

US Treasury Strip (maturity 104 weeks) |

|

52 week call on spot x-rate, Strike 290 |

|

52 week Put on spot x-rate, Strike 290 |

|

52 week Call on spot x-rate, Strike 310 |

|

52 week Put on spot x-rate, Strike 310 |

|

X-rate Future (500 bfx / 52 weeks) |

|

Money market (3% p.a.) |

The

currency crisis is not interest rate related, so you can assume that the

interest rates remain constant.

Trading

Objective

Your trading objective is

to earn as much grade cash as possible subject to the constraints imposed by

your firm upon your trading activities.

Earning

Grade Cash

Securities are exchanged

using market cash in a trading period that lasts for 52 weeks. Each 52 weeks is

referred to as one trading trial. Multiple independent trials will be

conducted.

That is, at the start of

a trial your initial endowment is either Type A or Type B, and an independent

exchange rate path (starting from the spot lot price of around 300).

If

at the end of any trial you have a closing balance of $4,500,000 market cash

you will earn $20 grade cash. If you

have a closing balance of market cash that is lower than $4,500,00

you will earn $0 grade cash. Any amount

of market cash that is greater than $4,500,000 and less than or equal to $100,000,000

earns grade cash as follows:

![]()

Above

$100,000,000 market cash earns the maximum of $402 grade cash for one trial.

Trading

is conducted over a number of independent trials and a record of your

cumulative grade cash is maintained.

Linking to the

Trading Support Spreadsheet for Trading Case XR2

Download the trading support spreadsheet for XR2

(just below the ftsTrader link) from the Virtual

Classroom page and open it in Excel.

Note: Read

carefully the appropriate Excel settings from the Virtual Classroom section

where you download the XR2 support spreadsheet from.

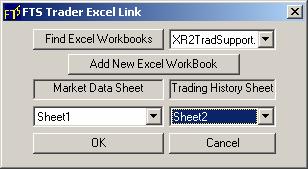

Launch the FTS Trader and link to the market. In FTS Trader click on the File menu and

select Excel Link from the sub menu items.

The following screen will pop up.

Select the spreadsheet titled XR2TradSupport and be sure to select Sheet

1 as the Market Data Sheet and Sheet 2 as the Trading History Sheet as depicted

below:

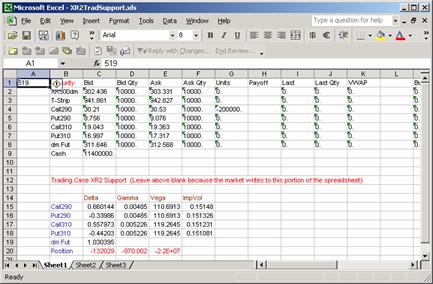

Click OK and the spreadsheet is automatically linked

to the market. By giving focus to the

spreadsheet (i.e., resize so it is on the same screen as your trading window),

you can see your position greeks

update in real time. The spreadsheet

support is illustrated below:

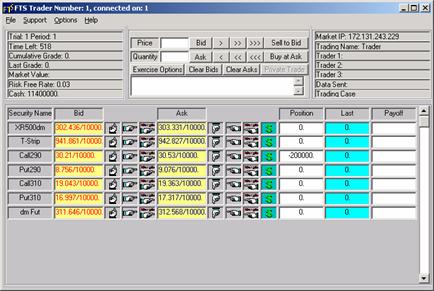

Corresponding

Trading Screen in the FTS Trader

Appendix

Trading Tips for Trading XR2

In

trading case XR2 you are a short term “news trader.” You have information that lets you form a

“market view” about the short term price behavior of the underlying exchange

rate. In XR2 the price of the underlying

exchange follows the geometric Brownian motion process assumed by Black and Scholes with one important difference. During the trading period at least one

significant economic news event will occur that will result in the price of the

exchange rate taking a jump. However,

you do not know when the jump will take place or it’s

magnitude and direction. In addition,

there may be more than one significant jump (but there will be at least

one). Unlike the real world you do not

face any liquidity or capital constraints.

You

have an initial position in an option that you cannot trade, but you can trade

the remaining derivatives (option and futures).

As a result, your task is to manage your trading strategy so that it

makes money if your view of the market is correct. At any time if you want to lock in your

trading gains you can also manage the delta of your position. By linking to the XR2 support spreadsheet

(you can download this from the Virtual Classroom page immediately below where

you download the FTS Trader from).

Why Delta?

Delta

is a measure of the dollar sensitivity of your position to changes in the

underlying (i.e., the exchange rate).

Formally, the delta of a derivative security is the partial derivative

(i.e., calculus) of the derivative security’s price w.r.t.

a change in the underlying asset price.

The delta of each security and your position’s delta are provided in the

support spreadsheet in real time.

Excel Note for FTS Trader: If Excel is set

to Automatic Calculate (Tools, Options, Calculations, Automatic) and you link

FTS Trader to this spreadsheet, it will automatically recalculate your position

delta whenever the exchange rate changes in XR2.

By

trading the options and futures you can manage your position delta to be

approximately zero, positive or negative.

For the case of a zero position delta your position’s value will be

relatively insensitive to shifts in the underlying exchange rate. If you assume a large positive position delta

your position will be very sensitive to shifts in the price of the underlying

(with increasing sensitivity the larger your position delta is). That is, if the underlying exchange rate

increases so does your position’s value and if the underlying exchange rate

decreases your position value will decline.

Finally, if you assume a large negative position delta then the value of

your position responds in the opposite way to the change in the exchange

rate. That is, if the exchange rate

increases your position’s value decreases and vice versa.

Finer points: Your position

gamma is a measure of how sensitivity your position delta is to changes in the

underlying. Formally, gamma is the

partial derivative (in calculus) of the derivative security’s delta w.r.t. the underlying asset price (i.e., the second partial

derivative w.r.t. the underlying asset price). In the field, suppose a dealer is hedging the

exchange rate risk by maintaining an approximate delta neutral exposure (i.e.,

position delta equals 0). If a dealer

maintains a gamma sensitive (i.e., large position gamma) position they must

adjust delta frequently and by larger amounts to maintain a zero position

delta. If a dealer maintains a gamma

insensitive position (i.e., approximately zero position gamma) then this

reduces the frequency and size of delta adjustments that need to be made to

maintain a zero position delta. In practice

by reducing the size and frequency of having to adjust your position’s delta

results in a source of significant transaction cost savings.

Finally,

your position Vega is a measure of how sensitive your position is to

volatility.

Inferring Information from Implied

Volatility Estimates: You should monitor the implied volatility in

your spreadsheet because prior to a crisis you will observe in this trading

case that implied volatility makes a significant initial jump. After the first jump it will then jump again

and so you should think about how you can adjust your trading strategies to

exploit this information.