Applying Markowitz diversification and the single period Capital Asset Pricing Model (CAPM)?

Markowitz diversification applied in it's traditional form has not been embraced by practitioners. In the the set of lessons on building portfolios and related results from empirical work the traditional application does not appear to be robust in the face of dynamic risk and return behavior.

In the single period CAPM investors are rewarded for assuming general market or systematic risk. In this model, shifts in the minimum variance frontier are not considered over time (because only one period exists) and thus no additional drivers of systematic risk are predicted. In the real world the intertemporal behavior of risk and return needs to be taken into account when building a portfolio.

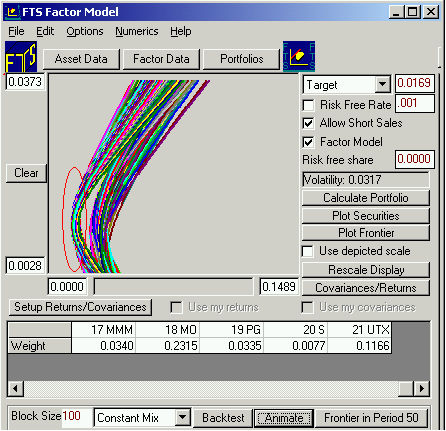

In this current lesson we examined using multiple factors to do this --- a yield curve factor, an equity premium factor as well as the two Fama and French factors. First it was demonstrated that these factors had a significant impact upon the scatter plot behavior of the minimum variance frontier, as depicted above. That is, estimates of the minimum variance frontier stabilized over time.

The next issue considered was whether constructing a portfolio from a more stable estimate of the minimum variance frontier had a positive impact upon realized portfolio performance? From the results of backtesting experiments using factors had a significant and positive impact upon the design and implementation of a portfolio.

In this lesson this positive impact resulted from exploiting factors designed to provide a better estimate of the variance covariance matrix of returns. That is, by working on risk. In the lesson we still relied upon historical averages for predicting expected return, and so this dimension of the problem was not considered. In future lessons we will examine the problem of forecasting expected return directly using fundamentals.