Realized versus Expected Returns?

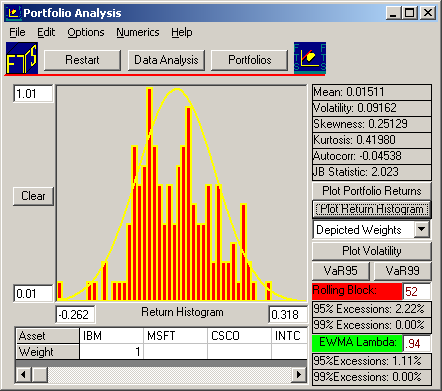

Financial assets are held for the return they expected to provide. The realized return distribution from monthly price data 1990-2001 is depicted in the above image (source: FTS Portfolio Returns Module). You can observe the average monthly return from IBM shares was 1.51% over this period of time (18.13% annualized).

A major part of any investment problem, however, is to assess the expected return from investing in the asset as opposed to past realized returns. In this lesson we focus on the former problem --- forecasting expected return.

To compute the expected return we need to first assess the intrinsic value of the stock. To forecast intrinsic value we apply the two stage abnormal growth model to dividends estimated as free cash flows to equity. The latter is useful because it covers firms that do pay dividends as well as firms that don't. In addition, it covers firms that substitute paying dividends with repurchasing stock on the open market using their free cash flow. This latter strategy is designed to exploit differential tax treatments of dividends versus capital gains in the hands of stock holders.

So for these reasons and more the free cash flow to equity approach is a preferred measure of dividends.

What is free cash flow to equity?

In 1939 John R. Hicks defined an economic concept of income as:

"The maximum value one can consume during the week and still expect to be as well off at the end of the week as at the beginning"

The concept of economic income is different from the accounting (accrual) concept of income because the latter has a capital maintenance ex post measurement orientation, whereas the Hicksian concept has a value maintenance ex ante (expectation) orientation. As a result, for the task of estimating intrinsic value the economic concept of income is better suited, whereas for contracting purposes the accounting concept of income is better suited.

The dividends paid by a stock in practice are paid from retained accounting earnings so that legal concepts of capital are maintained. Free cash flow to equity on the other hand is a concept about potential dividends and economic income. A firm's free cash flow to equity is the cash generated over the period that could be paid out as a dividend without affecting the beginning period value of the firm's operations and growth opportunities.

When estimating Free Cash Flow to Equity we usually start with the accounting financial statements and accounting income. We then make adjustments designed to estimate the dividends that could be extracted by stock holders without influencing their future "well offness" (i.e., maintaining the firm's growth and operations in tact).

What is Intrinsic Value?

In this lesson we define intrinsic value of the firm's stock as the present value of future free cash flows to equity (FCFE) discounted back at the firm's cost of equity capital.

We will adopt a two stage abnormal growth model to assess intrinsic value. This model assumes that FCFE grows at some abnormal growth rate for a finite period of time, and then at a normal rate in perpetuity thereafter. The cost of equity capital can be different across stages.